I've been keen on

investing in natural gas for well over a year, and the timing hasn't been right until now. But with natural gas spot price dropping below 2 dollars per

million British thermal units (MBTU) yesterday, and hitting a 14-year low, I thought I might deal with this investment idea again.

First let's make the case for investing in US natural gas.

The best time to buy commodities is when they are depressed. Let's have a look at US natural gas for the last 15 years (Source: IndexMundi.com)

The price is now back to 1997/1999 levels, right before the start of the massive commodities bull market and massive monetary inflation by central banks do not appear to be affecting natgas price.

If you think a 15-year low might be a good investment opportunity, what about an inflation adjusted 36-year low?

This chart was updated in January 2012, when natural gas was still above 2 USD per MTBU and it has since dropped to 1.98 USD per MBTU, so we are at least at a 36-year low (or very close to it) when adjusted with official inflation numbers.

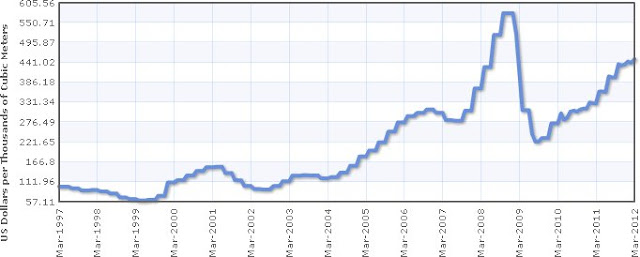

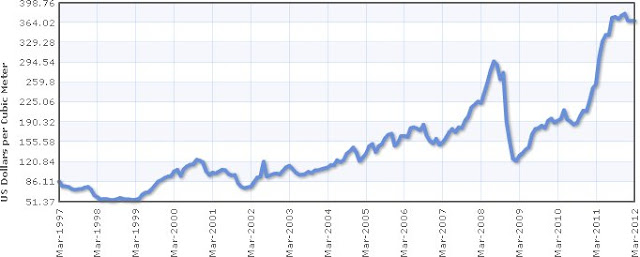

Pundits explains the price is low because of the glut of natural gas attributed to new technologies such as fracking, and this is certainly a very good point. But there is another aspect which is very bullish for US natural gas: international gas market. Russian natural gas and Indonesian LNG are still in a upward trend, and currently Russian natural gas is over 6 times more expensive than US natural gas as shown in the 15-year charts below (Source: IndexMundi.com).

|

| Russian Natural Gas (1997-2012) |

|

| Indonesian LNG (1997-2012) |

Natural gas is not has easy to transport as crude oil for example, but one of the issue is the lack of LNG terminal with the ability to export liquefied gas to international markets which would increase the price of natural gas in the US and help decrease the cost of natural gas overseas. According to Wikipedia, there is only one liquefaction terminal (for export) in Alaska for the whole US, but there are 13 regasification terminals (for import). There are 2 proposed liquefaction terminals in Louisiana and Oregon. Once completed, the US will be able to export more natural gas and hopefully take advantage of the differential between local and international prices.

Finally, Crude Oil (WTI) to Natural Gas price Ratio

stands now at over 50, whereas the historical norm has been around 8 to 10. See chart below (Souce: stockcharts.com)

So that means for a given amount of energy natural gas is about 5 times cheaper than crude oil. In reality, this is obviously not that easy as those 2 fuels are not interchangeable, but companies may start to invest more in power plant and transportation that can accommodate natural gas.

Now we have made the case to invest in natural gas, let's see how it can be done

There are some ETF to invest in Natural Gas such as UNG (USA) that are supposed to track natural gas price. However, their cost

(due to diverse costs and contango) is prohibitive so that I would really advise

against investing in those, unless you are able to correctly guess the price of

Natgas within 3 months.

Those types of ETF will go to zero by design.

You could potentially invest in companies such as Chesapeake or SandRidge Energy (

SD), but if natural gas stays too low for too long some of those companies may go bankrupt and you'd lose all your investment. If you have enough capital, you could buy a list a companies involved in natural gas extraction and exploration, but for most of us, the simplest is to invest in mutual funds or ETF.

First Trust ISE-Revere Natural Gas Idx (

FCG) is an ETF tracking

ISE-REVERE Natural Gas Index which is composed of the stock of companies dealing with natural gas production and exploration.

Let's see how FCG fared in the last five years (Source: Yahoo Finance).

The first obvious thing is that it tracks natural gas rather poorly. FCG followed the price hike in 2008, but since 2009 it has more or less tracked the performance of the S&P 500. This makes me a little uneasy to buy FCG right now, but in case of further weakness (at least below 15), it might be interesting to start buying this ETF to have some (limited) exposure to natural gas.

I'm not fully satisfied with this method of investing in natural gas, but it's the best I've found so far. If you have better ideas, let me know.

I've also seen some companies are selling Oil and Gas Royalty Rights, but I have not checked this into details yet, as it may not be easy to access such investment for oversea investors.