Sprott Asset Management published their monthly newsletter Market at Glance (October 2011) entitled "Oil or Not, Here They Come".

First, they explain that oil has been mostly absent from recent financial headlines, but availability and price of crude oil remains a key factor in world growth:

While the recent clamor over EU solvency and weak global growth has temporarily displaced its media attention, oil’s crucial importance to the world economy has not dwindled in the slightest. Oil remains the world’s greatest single energy source today

...

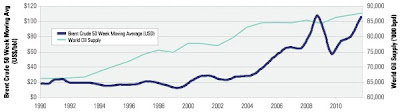

By historical standards, the world has been coping with constrained oil production and high oil prices for most of the past six years. This tightness in oil supply has been a significant factor limiting global growth, and it would appear that no matter what financial solutions are eventually engineered by our politicians, global growth will remain significantly restricted by the real economy’s ability to produce oil. Limited global supply growth means that the Western world now faces significant competition for oil from emerging markets whose citizenry are willing to work much harder for far less. This will continue to result in a narrowing gap of per capita consumption between emerging and developed economies as the emerging economies continue to gain relative economic strength, wage growth, currency appreciation and purchasing power. We believe strategic investments in oil producers and service companies will offer an effective way to profit from this trend.

Then then mainly focus on the lack of oil production growth:

Global oil production has grown very little (since 2005), appreciating by a mere 2% in total production. This production plateau generated the 2008 oil price spike to nearly $150 per barrel. Subsequently, despite the economic stagnation experienced by developed economies, the price of Brent Crude Oil has averaged over $78 per barrel, four times higher than the ~$18 average that Brent traded at in the 1990s.

and that the

International Energy Agency (IEA) and the

U.S. Energy Information Administration (EIA) have had to consistently reduce their production forecasts over the years as you can see in the chart below with forecast for 2015 and 2020:

They also shows other charts with price forecast made in 2002 with price ranging between 15 to 30 USD (high price scenario) between 2002 and 2025, in 2009 they revised this with a price range of 50 to 200 USD. (2008 USD).

In the next section, they look at the causes of high oil price namely supply constraints, high production cost, middle east export are riskier and costlier and increased demand from emerging countries:

Supply Constraints.

First, and most importantly, global supply is struggling to grow because we are not finding and bringing into production any new "super giant" oilfields. This reality was well documented by the EIA in a study it published in 2008.3

The EIA study revealed that the largest 1% of oilfields (798 total fields) in the world account for over 50% of global production.

What has been discovered and brought into production in the past few decades are smaller fields, which normally have higher decline rates. As these new smaller fields replace production from larger fields, and older larger fields age, we can expect the global observed decline rate to increase from the current estimated rate of 6.7% (or 4.7 million barrels per day annually).

High Production Costs.

Oil prices are also high due to rising production costs, and it’s worth noting that new production sources, such as offshore, tar sands and other unconventional sources are amongst the highest cost producers today... As a result, it is becoming clear to many industry analysts that current oil production cannot be sustained under $75 a barrel and the price required to sustain production seems destined to continually rise.

Middle East Exports are Increasing in Cost and Risk.

The so-called "Arab Spring" uprisings in countries such as Egypt and Libya are forcing these and other major oil producing nations to spend more of their oil revenue on social assistance programs. For example, as a result of newly announced social spending in Saudi Arabia, it is forecasted by The Institute of International Finance, Inc. that the budget balancing price of Saudi oil will jump from $68 per barrel in 2010 to $85 per barrel in 2011 and then continue to rise, but at a slower pace, to $110 per barrel by 2015.

Increased Demand from Emerging Markets.As globalization continues, we can expect job growth to be higher in countries where the citizenry are willing to work harder for less. This roughly characterizes the emerging market countries which for the most part are also large exporters of goods and services, run significant trade surpluses and have strengthening currencies. These factors enable them to continue to increase their per capita and total oil consumption. Conversely, higher wage Western nations are fighting rising unemployment, trade deficits, weakening currencies and, consequently, are being forced to reduce their oil consumption.

They also spend a large part of the letter comparing the US and China in terms of economic growth and oil consumption.

To conclude, they recommend that western investors hedge themselves against declining purchasing power and oil consumption by buying oil producer and service companies:

For North American workers and investors, one way to hedge against a decline in living standards is to use your current relative advantage in oil purchasing power to accumulate oil reserves that will be developed in the future. This purchasing power advantage, currently evident in the time a worker in the West must work to earn a barrel of oil, will eventually dissipate, as world labour markets recalibrate and shift wealth from West to East....

The recent market decline and ongoing volatility is affording investors with an opportunity to invest in oil producers and service companies, in particular junior and mid-cap companies, at attractive valuations. Equities are pricing in much lower oil prices over the long-term. Our view is that while there may be additional volatility in the crude oil price in the short-term, long-term pricing will remain high and equity prices will rise to correct this disconnect.

You can subscribe to

Sprott Asset management's Market at Glance newsletter free of charge or download the PDF version.

My take is that you although you can invest in oil producer such as Exxon, BP and the like, you could also invest in Oil Producing countries via

Market Vectors Gulf States Index ETF (MES) for example. However, since supply will go down overtime, that means reserve of oil companies will also go down so this is a negative for such companies although crude oil price is likely to increase. Another way would be to invest in Crude Oil directly either buy buying commodities futures or ETF, but be careful which one you choose (e.g. avoid USO at all cost).